How to process travel expenses in 1s 8.3. Accounting info

Almost every organization in its economic activity faces the need to send employees on business trips. For an employer, an employee’s business trip involves performing a number of actions. Firstly, the fact of being sent on a business trip must be properly documented. Secondly, the employer is obliged to retain the employee’s average earnings for the period of a business trip and reimburse the employee for expenses. Thirdly, business travel expenses must be taken into account for tax purposes. How to correctly carry out all these operations in the 1C: Salary and Personnel Management 8 program, says E.A. Gryanina, leading specialist of IT-Basis LLC.

(form No. T-10a)

(form No. T-10)

Rice. 1

Please note

Please note

Documentation of business trips

The procedure for formalizing the assignment of employees on business trips is established by the instruction of the Ministry of Finance of the USSR, the State Committee for Labor of the USSR and the All-Union Central Council of Trade Unions dated 04/07/1988 No. 62 “On business trips within the USSR” (hereinafter referred to as the Instructions on Business Travel, valid to the extent that does not contradict the Labor Code of the Russian Federation).

To document business trips, the following types of primary documentation forms, approved by Decree of the State Statistics Committee of Russia dated January 5, 2004 No. 1, can be used for personnel records.

Service task and report on its completion

(form No. T-10a)

It is used for registration and accounting of official assignments for sending on a business trip, as well as a report on its implementation.

The official assignment is signed by the head of the structural unit in which the posted worker works, approved by the head of the organization or a person authorized by him for this, and on its basis an order (instruction) is issued to send him on a business trip.

Upon returning from a business trip, the employee draws up a report on the work performed during the business trip, which is agreed upon with the head of the structural unit and submitted to the accounting department.

Drawing up a work assignment and a report on its implementation is not a mandatory requirement of the Business Travel Instructions, but its presence will be useful to confirm the production nature of the business trip in order to be able to accept business trip expenses for profit tax purposes.

Order (instruction) on sending an employee

on a business trip (forms No. T-9 and No. T-9a)

They are used to register and record the assignment of an employee (or employees) on a business trip. Filled out on the basis of an official assignment, signed by the head of the organization or a person authorized by him to do so.

Travel certificate

(form No. T-10)

It is a document certifying the time spent on a business trip on the territory of the Russian Federation or a CIS country, upon entry and exit to which, according to intergovernmental agreements, a mark on crossing the state border is not affixed.

The travel certificate is issued in one copy based on the order to go on a business trip and is given to the employee. At each destination, notes on the time of arrival and departure are made on the travel certificate, which are certified by the signature of the responsible official and the seal. After returning from a business trip, the travel certificate is provided to the accounting department along with the employee’s advance report and documents confirming the expenses incurred. A travel certificate may not be issued if the employee must return from a business trip to his place of permanent work on the same day on which he was sent. Also, a travel certificate is not issued when traveling abroad (except for the above-mentioned CIS countries).

In accordance with paragraph 2 of the Instructions on Business Travel, if an employee is issued a travel certificate, then issuing an order for the organization to send him on a business trip is optional, but can be made by decision of the manager.

According to the explanations of the Ministry of Finance of Russia, an organization can independently establish a list of documents that are the basis for sending an employee on a business trip, which, in particular, can be a business trip order and (or) the issuance of a travel certificate. The preparation of two documents on one fact of economic activity, in the opinion of the financial department, is optional (letter of the Ministry of Finance of Russia dated December 6, 2002 No. 16-00-16/158).

Thus, when sending employees on a business trip to the territory of the Russian Federation, it is enough to issue a travel certificate; in this case, an organization order does not need to be issued. Sending employees on a foreign business trip should be formalized by an order from the organization, since for such business trips a travel certificate is not issued.

The program "1C: Salary and Personnel Management" allows you to draw up all the unified forms of primary documents discussed above related to sending employees on business trips: No. T-9, No. T-9a, No. T-10 and No. T-10a.

Registration of the fact of sending an employee or a list of employees on a business trip is carried out in the program using the document of the personnel accounting subsystem “Business trips of organizations” (see Fig. 1).

Rice. 1

The on-screen form of the document indicates the destination: the country, city and organization to which the workers (employee) are sent, as well as the details of the document that is the basis for the business trip (official assignment or other document).

The tabular part is filled in with a list of employees sent on a business trip.

The purpose of the business trip (the content of the job assignment) is indicated in the form of an arbitrary text string for each employee. Additionally, to print out the order, you can specify the source of financing for business trip expenses.

To obtain printed forms of a travel certificate, an order to send on a business trip and a work assignment, you must use the drop-down submenu of the “Print” button on the lower command panel of the document form.

Please note that the Labor Code of the Russian Federation prohibits sending pregnant women on business trips (Part 1 of Article 259 of the Labor Code of the Russian Federation), workers under the age of 18 (Article 268 of the Labor Code of the Russian Federation), and employees during the period of validity of the apprenticeship contract - on business trips not related to apprenticeship (Part 3 of Article 203 of the Labor Code of the Russian Federation).

It is allowed to be sent on business trips, but only with written consent and subject to familiarization in writing with your right to refuse to be sent on a business trip (Article 259 of the Labor Code of the Russian Federation):

- women with children under three years of age, provided that this is not prohibited by medical recommendations;

- workers with disabled children or people with disabilities from childhood until they reach the age of 18;

- workers caring for sick members of their families in accordance with a medical report;

- men raising minor children without a mother, as well as guardians and trustees of minors (Article 264 of the Labor Code of the Russian Federation).

For each employee, the document indicates the start and end dates of the business trip (taking into account the time spent on the road), the number of days on the road is entered in a separate field in the row of the tabular section.

Please note, that in accordance with paragraph 4 of the Instructions on Business Travel, the duration of a business trip within the Russian Federation should not exceed 40 calendar days, not counting the time spent en route. The duration of the business trip for workers, managers and specialists sent to perform installation, commissioning and construction work should not exceed one year. There is no deadline for which an employee can be sent on a business trip abroad.

Payment for time spent on a business trip

While on a business trip, the employee retains his average earnings (Article 167 of the Labor Code of the Russian Federation).

The average salary is calculated in accordance with the Regulations on the specifics of the procedure for calculating the average salary, approved by Decree of the Government of the Russian Federation dated April 11, 2003 No. 213.

To accrue the employee's retained average earnings in the program "1C: Salary and Personnel Management 8" the document "Payment based on average earnings" is intended. The document can be created, calculated and posted automatically based on the document “Business trips of organizations” using the processing “Analysis of Absences” (Fig. 2). You can call processing directly from the document form “Business trips of organizations” by clicking the “Open accruals” button.

Rice. 2

By default, to calculate payment for the time spent on a business trip, the predefined calculation type “Payment based on average earnings” is used (indicated in the “Calculation type” field of the document form). At the same time, in terms of calculation types “Basic accruals of organizations”, a custom type of calculation for performing accruals can be described (for example, if it is necessary to make special adjustments to the accounting for a particular type of business trip).

Data for calculating average earnings are indicated in the tabular part of the document on the “Calculation of average earnings” tab, summarized by type of earnings:

- basic income;

- bonuses that are fully taken into account in average earnings;

- bonuses partially taken into account in average earnings;

- annual bonuses fully taken into account in average earnings;

- annual bonuses, partially taken into account in average earnings.

When calculating the document, this data is generated automatically based on the settings of basic accruals for calculation types from the “Average Earnings” calculation types plan, data on the employee’s accruals, time worked and standard time, as well as data on the indexation of the employee’s wages for the billing period.

Data on basic earnings and non-annual bonuses are collected separately for each month of the pay period. Basic earnings amounts fall into the month of the billing period for which they are accrued. Premium amounts are included in the month of accrual, regardless of the period for which they were accrued.

Annual premiums are included in the base only if they are accrued for the calendar year preceding the date of the event, regardless of the month in which the accrual was made.

The billing period is considered to be 12 calendar months preceding the period of saving the average earnings, unless otherwise determined by the settings of the type of calculation selected for paying for the time spent on a business trip in the document.

To calculate the accrual result, the average daily earnings are calculated, and for employees with summarized working hours, the average hourly earnings, which are multiplied by the number of working days (hours) according to the employee’s schedule falling during the business trip. The results of calculating payment for the duration of a business trip are placed on the “Accruals” tab of the document.

If at the end of the month the employee’s business trip has not yet ended, but he needs to accrue payment for the time of the business trip, then as the payment period in the document “Payment according to average earnings” you should set the period from the start date of the business trip to the end date of the month and calculate the document . Next month, payment is calculated for the second part of the business trip period - from the beginning of the month to the day of return from the business trip. The second part of the period of being on a business trip must be paid based on the same amount of average earnings as the first part. To do this, you need to copy the “Payment based on average earnings” document registered last month, indicate the corresponding payment period and calculate only the accruals, without recalculating the average earnings, i.e. you should use the “Calculate accruals” item in the submenu of the “Calculate” button.

In accordance with paragraph 9 of the Instructions on Business Travel, when a person working part-time is sent on a business trip, the average earnings are retained at the place of work in the organization that sent him on business. If you are sent on a business trip simultaneously for your main and combined work, the average earnings are maintained for both positions.

Thus, in order to resolve the issue of the need to pay for the time spent on a business trip for part-time workers, it is necessary to consider the purpose of the business trip - with the performance of duties for what position (place of work) it is associated with.

If an employee is sent on a business trip to perform duties only at his main place of work, then his absence from the part-time workplace must be registered in the program using the document “Absenteeism in Organizations.”

Reimbursement of expenses incurred by an employee in connection with a business trip

The list of expenses that the employer is obliged to reimburse to an employee sent on a business trip is established by Article 168 of the Labor Code of the Russian Federation and includes:

- travel expenses;

- expenses for renting residential premises;

- additional expenses associated with living outside the place of permanent residence (per diem);

- other expenses incurred by the employee with the permission or knowledge of the employer.

The procedure and amount of reimbursement of expenses related to business trips are determined by a collective agreement or local regulations of the organization. At the same time, it should be taken into account that for employees of organizations financed from the federal budget, reimbursement of expenses associated with business trips is made in accordance with the norms established by law.

For other organizations, the norms and procedures for reimbursement of travel expenses are established only for tax purposes.

Before leaving on a business trip, a posted employee is given a cash advance within the limits of the amounts due for travel, expenses for renting accommodation and daily allowances.

Within three days upon returning from a business trip within the territory of the Russian Federation (or within 10 calendar days from the end date of a business trip outside the Russian Federation), the employee is required to submit an advance report on the amounts spent in connection with the business trip and make a final payment for them.

Settlements for reimbursement of travel expenses for employees sent on business trips are not registered in the 1C: Salary and Personnel Management 8 program, since they do not relate to payroll calculations.

At the same time, unspent and not returned timely advances issued in connection with a business trip may be withheld from the employee’s salary. The deduction is registered in the program "1C: Salary and Personnel Management 8" using the document "Registration of one-time deductions of employees of organizations" (Fig. 3). The corresponding type of deduction must be described in the plan of calculation types "Deductions of organizations" with the calculation method "Fixed amount".

Rice. 3

Taxation of travel expenses for personal income tax and unified social tax

According to paragraph 3 of Article 217 and subparagraph 2 of paragraph 1 of Article 238 of the Tax Code of the Russian Federation, all types of legally established compensation payments related, in particular, to reimbursement of travel expenses, are not subject to personal income tax and unified social tax.

When the employer pays the taxpayer expenses for business trips both within the country and abroad, daily allowances paid within the limits established in accordance with current legislation, as well as actually incurred and documented targeted expenses for travel to the destination and back, are exempt from taxation. fees for airport services, commission fees, expenses for travel to the airport or train station at places of departure, destination or transfers, for luggage transportation, expenses for renting living quarters, paying for communication services, obtaining and registering a service foreign passport, obtaining visas, as well as expenses associated with the exchange of cash or a check at a bank for cash foreign currency.

Please note that from January 1, 2008, Federal Law No. 216-FZ of July 24, 2007 establishes maximum daily allowance rates exempt from personal income tax: up to 700 rubles for each day of a business trip in the Russian Federation and up to 2,500 rubles for each day of being on a foreign trip business trip.*

Note:

* Read more about these changes to the Tax Code of the Russian Federation in the article by L.P. Fomicheva “The Tax Code of the Russian Federation has been corrected again” in issue 9 (September) of “BUKH.1S” for 2007, p. 6.

For the purposes of calculating personal income tax in the program “1C: Salary and Personnel Management 8”, excess daily allowances, undocumented transportation expenses and expenses for renting residential premises, as well as other expenses not expressly mentioned in the Tax Code of the Russian Federation, reimbursed in connection with sending on a business trip , must be accrued to the employee in the form of non-monetary income. The accrual is made by the document “Registration of one-time accruals to employees of organizations.” The types of calculations by which income is calculated must be described in terms of the types of calculation "Basic accruals of organizations" or "Additional accruals of organizations" with the checkbox "Is income in kind" checked (Fig. 4).

Rice. 4

For the purposes of calculating personal income tax, such income is accounted for under code 4800 “Other income”.

For the purposes of taxation of UST and insurance contributions to the Pension Fund for organizations that pay income tax, the accrual type form is set to the value “Not subject to taxation of UST, contributions to the Pension Fund in accordance with paragraph 3 of Article 236 of the Tax Code of the Russian Federation (payments from profits).” For organizations applying special tax regimes, i.e., not paying corporate income tax, such accruals should be subject to mandatory contributions pension insurance. For them, as a method of taxation of UST and contributions to the Pension Fund, the value “Taxed by UST, contributions to the Pension Fund as a whole” should be specified (in fact, in the program in this case, only contributions to the compulsory pension fund will be charged).

The accruals in question are also subject to contributions for compulsory accident insurance, which is indicated accordingly in the accrual type form.

When determining the amount of excess daily allowance, it should be borne in mind that the norms are established in the amount of payments for each day the employee is on a business trip, including the time spent on the road. The day of departure on a business trip is considered to be a calendar day (up to 24 hours inclusive) during which a train, plane, bus or other vehicle departs from the place of permanent work of the business traveler, and the day of arrival is a calendar day (up to 24 hours inclusive) during which the transport the product arrives at the place of permanent work. If a business trip lasts one day, per diem is not paid. If the place from which the vehicle departs is located outside the boundaries of the locality in which the organization is located, then when determining the days of departure and arrival, the time required to travel to the place of departure is taken into account vehicle. The same procedure applies if the business traveler has the opportunity to return daily to his place of permanent residence (the availability of such an opportunity is decided by the employer in each specific case).

If an employee gets sick on a business trip

According to paragraph 16 of the Instructions on Business Travel, in the event of temporary incapacity for work of a posted worker, he is reimbursed on a general basis for the costs of renting living quarters (except for cases when the posted worker is undergoing hospital treatment) and is paid daily allowances for the entire time he is unable to do so due to his condition. health, begin to carry out the official assignment assigned to him or return to his place of permanent residence, but not

over two months. Days of temporary incapacity for work are not included in the business trip period.

The temporary disability of a posted worker, as well as the inability for health reasons to return to his place of permanent residence, must be certified in the prescribed manner.

During the period of temporary incapacity for work, the posted worker is paid a temporary disability benefit on a general basis.

The reflection of such cases in the 1C: Salary and Personnel Management 8 program depends on whether payment for the business trip period was registered in the program at the time of accrual of temporary disability benefits, and if so, in what billing period- current or one of the past.

If the program first accrues sick leave, and then enters payment for a business trip, then when calculating the accrual for the time of a business trip, the program will automatically take into account the period of temporary disability: the employee will not be paid for the business trip for sick days.

If payment for the business trip was already registered earlier in the current month, then after accrual of sick leave, the document for calculating payment for the business trip “Payment based on average earnings” must be recalculated, which the program will remind you of on the current task panel.

If payment for the business trip was made in one of the previous periods, then when calculating accrual for sick leave, the amounts of payment for the business trip falling on sick days will be automatically reversed (Fig. 5).

Rice. 5

For the described behavior of the program, the list of displacing payment types for business trips (“Payment based on average earnings”) must include the types of calculations used to pay for temporary disability benefits (“Payment for sick leave” and “Payment for sick leave for work-related injuries.” ).

To accrue travel allowances in 1C ZUP 3, you need to set the settings for payroll calculation standards (Fig. 1). The system automatically creates accrual types “Business trip” and “Business trip (intra-shift)”.

Rice. 1. Set up payroll

When you specify the “Pay for long business trips monthly” parameter in the settings, the switch will automatically be set to the “Pay for business trip at the end of the month” position when creating the “Business trip” document.

Calculation of travel allowances in 1C ZUP for an employee is carried out using the “Business Trip” document. The document is multifunctional, i.e. Working with a document is provided in 2 modes:

- The HR mode includes creating a document, filling out the business trip period, and posting the document (Fig. 2):

Rice. 2. “Business trip” in the personnel circuit

Rice. 2. “Business trip” in the personnel circuit

If the company conducts staffing table, then when conducting a business trip, on the “Main” tab, you must indicate the attribute “Free up the rate for the period of the business trip.”

When specifying the attribute “Part-time/intra-shift business trip”, the field for indicating the hours of intra-shift business trip and the preempted planned type of time becomes active (Fig. 3):

Rice. 3. Intra-shift business trip

Rice. 3. Intra-shift business trip

If in the employee’s Pension Fund of Russia experience it is necessary to indicate the fact of his work on a business trip in an area with conditions different from the main place of work, then on the “PFR Experience” tab their value for the period of the business trip should be indicated (Fig. 4).

If a business trip is not included in the preferential period of the Pension Fund of Russia, then it is necessary to indicate the corresponding sign (Fig. 4).

Rice. 4. Tab “PFR Experience” of the “Business Trip” document

Rice. 4. Tab “PFR Experience” of the “Business Trip” document

- The calculator mode includes calculating the document, placing the document in the calculation circuit (Fig. 5):

Rice. 5. Document “Business trip” in the calculation outline

Rice. 5. Document “Business trip” in the calculation outline

When specifying the “Calculation approved” attribute, the document is considered approved in the calculation outline and allows you to reflect travel allowances in the 1C ZUP 3 system.

If the employee’s business trip is transitional from one month to another, then the “Payment for long-term business trip” block is available on the document form in the “Main” tab (Fig. 5).

If you specify the option “Pay the entire period of the trip,” the trip will be paid in full for the entire period and reflected in accounting in the current document.

If you specify the “Pay for business trip at the end of each month” attribute, the system will calculate the part of the business trip that falls on the month of accrual. In our example, the month of accrual is February 2017, there is 1 day of the business trip - 02/28/2018, and the amount is 2100 rubles (Fig. 5).

The remainder of the business trip will be calculated during the next payroll calculation in the document “Calculation of salaries and contributions” in March 2018 (Fig. 6).

Rice. 6. Accrual of part of the business trip in the document “Accrual of salaries and contributions”

Rice. 6. Accrual of part of the business trip in the document “Accrual of salaries and contributions”

If there are several types of calculations accrued by the “Business Trip” document, the system allows you to select the required accrual.

To calculate travel allowances in 1C ZUP, employees using the T-9a form must use the document “Group trip”. To reflect a business trip in accounting, entering the document “Group Travel” is not enough. After entering a group document, it is necessary to reflect the fact of a business trip with the “Business trip” documents. To simultaneously enter documents for all employees, you must click on the “Register absences” link under the tabular part. The document is multifunctional and works in 2 modes – personnel and settlement.

Travel expenses within normal and above normal limits

Expenses reimbursed by the employer to an employee during a business trip (Article 168 of the Tax Code of the Russian Federation) are reflected in the reporting of insurance premiums.

According to clause 2 of article 422 of the Tax Code of the Russian Federation, paragraph 12 of clause 3 of art. 217 of the Tax Code of the Russian Federation, expenses during a business trip are not subject to insurance contributions and personal income tax if they:

- Do not exceed 700 rubles for each day of a business trip within the Russian Federation;

- Do not exceed 2,500 rubles for each day of a business trip outside the Russian Federation.

If the employer sets daily allowances in a larger amount than specified in the Tax Code of the Russian Federation, then he will need to withhold personal income tax from the excess amounts and charge insurance contributions.

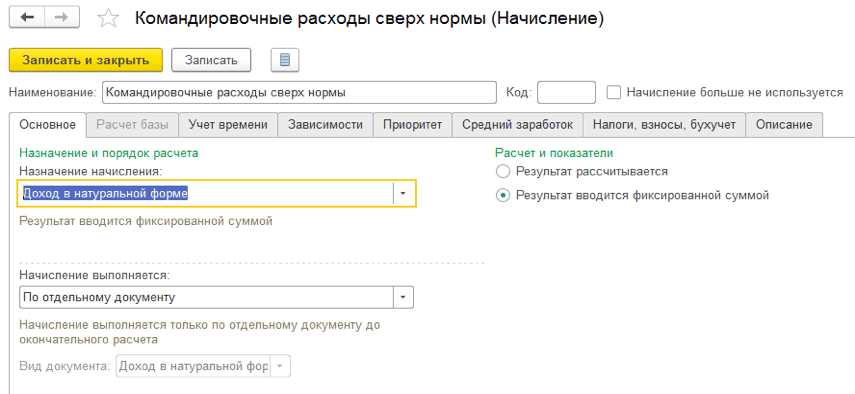

To display expenses on a business trip within normal limits in 1C ZUP 3, you must enter an accrual with the following settings (Fig. 7):

Rice. 7. Setting spending within normal limits

Rice. 7. Setting spending within normal limits

The accrual is carried out by the document “Income in kind” (Fig. 8):

Rice. 8. Expenses during the business trip are within the normal limits in the document “Income in kind”

Rice. 8. Expenses during the business trip are within the normal limits in the document “Income in kind”

To reflect expenses for a business trip period in excess of the norm in 1C ZUP 3, you must enter an accrual with the following settings (Fig. 9):

Fig 9. Setting up excess spending

Fig 9. Setting up excess spending

The accrual is carried out by the document “Income in kind” (Fig. 10):

Rice. 10. Expenses in excess of the norm in the document “Income in kind”

Rice. 10. Expenses in excess of the norm in the document “Income in kind”

The calculation of insurance premiums for travel expenses accrued in excess of the norm is carried out in the document “Calculation of salaries and contributions”.

Early return from a business trip

By decision of the manager, an employee may be recalled early from a business trip. This point is not regulated by law. The employer decides independently how to do this.

In the 1C ZUP 3 program there are 2 options for processing a return from a business trip:

- If the period is not closed, then the original document “Business trip” is corrected.

- If the period is closed, a business trip has been paid, or a document “Reflection of salaries in accounting” has been generated, then you must use the mechanism for correcting the document.

You must select one of the correction options:

- Enter the document-correction. The “Correct” link appears in the frame outline at the bottom of the document (Fig. 11). When you click on the link, a new document is created, and the corrected document is blocked. The tooltip “This document is a revision of another document” appears at the bottom of the new document. The calculator calculates the corrected document. The correction method is suitable for cases when the travel period changes.

- Reverse the document completely. A “Reverse” link appears in the calculation outline at the bottom of the document. When you click on the link, a “Reversal of Accruals” document is created (Fig. 12), and the corrected document is blocked. The correction method is suitable for cases of complete cancellation of a business trip.

Rice. 11. Correction of the document “Business trip” - personnel outline

Rice. 11. Correction of the document “Business trip” - personnel outline

Rice. 12. Correction of the document “Business trip” - design contour

Rice. 12. Correction of the document “Business trip” - design contour

Payment is recalculated based on the employee’s average earnings calculated at the time of departure on a business trip.

When a document-correction is carried out, the employee’s planned time according to his work schedule is entered in the time sheet.

At an enterprise, there are quite often situations when an employee needs to be paid for the period of work by average earnings in accordance with the Labor Code of the Russian Federation.

The most common case is payment for the period an employee is in business trip.

For this purpose, the 1C Salary and Personnel Management program provides a document ““.

You can find it in the program on the “Payroll calculation” desktop tab, “Payment based on average earnings” link, or in the main menu of the program, “Organization payroll calculation” -> “No-shows” -> “Payment based on average earnings.”

In the list of documents that opens, enter a new one using the “Add” button. A new document form opens:

Necessary details for calculation:

Organization (if a default organization is defined in the user settings, then when creating a new document it will be entered automatically);

Accrual month - the period in which the document will be registered;

An employee who is paid according to average earnings;

Start date of the period for maintaining average earnings (this date is important. When average earnings is registered during one period with several documents, as well as to clarify the billing period used to calculate average earnings);

Period of paid time: full-day or intra-shift.

To pay for a business trip, you need to set the switch to the “all day” position. In this case, the “from” and “to” details will become available, which must be filled in with the start date and end date of the trip, respectively.

If you set the switch position to “intra-shift”, you must fill in the date of payment based on average earnings and the number of hours of payment. But in our case we will not do this.

Below is the “Accrue” group of details. In the “type of calculation” attribute, you can select types of calculations calculated based on average earnings - full-day or intra-shift, depending on the position of the switch.

Select the calculation type “Payment by average”. In order to make sure that in the T-13 time sheet this type of calculation will be displayed correctly and it will be calculated as we need, you can open this type of calculation for viewing using the button located on the right side of the “Calculation Type” attribute magnifying glass

The form for setting up the payment type “Payment by average” will open. The calculation formula is described on the “Calculations” tab:

On the “Time” tab, make sure that the type of time is indicated correctly: “Unworked full shifts, as well as business trips.”

The type of time according to the working time use classifier is also set correctly: “ Business trip"(letter designation "K").

Let's close the calculation type form and start calculating our document. Click on the “Calculate” button, and if the database contains information about payroll for the previous 12 months, the system will automatically calculate both the average daily earnings and the calculation of payment based on average earnings during the business trip:

We can consider the details of calculating average earnings by going to the “Calculation of average earnings” tab:

As you can see, in addition to the basic monthly salary, the average earnings may also include various bonuses: fully or partially taken into account, indexed or not. In our case, there were no bonuses for the previous 12 months.

On the “Payment” tab, you can view the details of calculating the amount accrued based on the average.

The row in the tabular section displays the start and end dates of payment, the type of accrual, the number of days and hours paid, the result, and the start date of the event.

Below the table there is an information line with the total payment amount and the number of paid days.

We post the document (the “Post” button is located in the top command bar of the document form. In order to simultaneously post and close the document, the “OK” button is intended).

We will generate the document “Working time sheet” for May for employee Akimova.

Let's make sure that our business trip was displayed in it with the letter “K”. Please note that I entered the period from May 6 to May 9, i.e. 5 calendar days, but the program only paid for working days. This is correct, because weekends and holidays on a business trip are paid by the document ““.

Thus, in the 1C Salary and Personnel Management 8.2 program, it is introduced over time business trips.

Video tutorial:

One of the most common cases when employees at an enterprise are paid an average salary is when the employee is on a business trip. Each business trip is formalized by an order indicating the employee’s last name, first name, and patronymic; where is he going; purpose of the trip; period of being on a business trip. The period of stay is paid to the employee in accordance with the Labor Code (hereinafter referred to as the Labor Code) of the Russian Federation. In this article I want to clearly examine the topic of how to arrange a business trip for an employee in the 1C program.

Setting up a salary block in the 1C program

In order to pay salaries to employees, it is necessary to correctly configure the payroll accounting parameters. To do this, you need to log into the program as an employee who will set the necessary parameters with “Administrator” rights. In the main menu, open the “Salary and Personnel” section, then in the “Directories and Settings” block, find the “Salary Settings” item.

It is correct to establish in it, in accordance with the Labor Code of the Russian Federation and the Regulations on Remuneration of Labor, all the necessary parameters. If in the 1C program you do not find a document for accruing a business trip, then you need to create it; it will calculate the average earnings if the employee is on a business trip.

A document for calculating average earnings, when an employee is on a business trip, can be created by an accounting specialist; it is not so difficult, and it will not take much time.

To do this, go to the settings, to the “Accrual” block to create a document.

Click on the “Create” button, a window opens on the monitor screen in which you need to fill in (select, set a feature) the following positions:

Click on the “Create” button, a window opens on the monitor screen in which you need to fill in (select, set a feature) the following positions:

- Name;

- personal income tax;

- Insurance premiums;

- Income tax;

- Reflection in accounting;

- Included in the basic accruals for calculating the accrual " Regional coefficient" and "Northern Surcharge".

In the field:

In the field:

- “Name” can be written “Payment based on average earnings when the employee is on a business trip”;

- “Personal income tax”, set the “Taxed” attribute, indicating the “Income code”;

- “Insurance premiums”, select the type of income “Income entirely subject to insurance premiums”;

- “Income tax”, set the attribute “Taking into account as part of labor costs” and select the item for attributing expenses;

- “Reflection in accounting” select the method of reflection.

After that, click on the button:

After that, click on the button:

- “Record and close”;

- Or "Record".

Only after this can you calculate the average earnings while the employee is on a business trip

Maintaining average earnings while an employee is on a business trip in the 1C program

To draw up a document in 1C that would allow us to calculate the average earnings during a business trip, we need to go to the main menu, the “Salaries and Personnel” section, select the “Salaries” block, and in it the “All accruals” position. A journal will appear on the screen, in which all accruals for employees for previous periods will appear. We create an accrual for the current month, to do this, click on the “Create” button and select the “Salary accrual” position.

In the accrual document, you must fill in the following fields in the document header:

In the accrual document, you must fill in the following fields in the document header:

- Month of accrual;

- Organization;

- Subdivision.

Going to the tabular part of the document, open the “Accrual” tab. From the directory, select the employee and the type of accrual that you created earlier, “Payment based on average earnings when the employee is on a business trip,” enter the days of the business trip, the hours, and display the result. Afterwards we carry out the document by clicking on the “Post” button and close it.

You can create payroll documents for each employee of the organization or for all employees. Then to do this you need to click on the “Fill” button.

It is necessary to remember that arranging a business trip for an employee is associated not only with the calculation of average earnings, but also with the documentation of sending the employee on a business trip, with the issuance of cash in the report, with the preparation of an advance report, with the return of funds and others.

It is necessary to remember that arranging a business trip for an employee is associated not only with the calculation of average earnings, but also with the documentation of sending the employee on a business trip, with the issuance of cash in the report, with the preparation of an advance report, with the return of funds and others.

Hello dear blog readers. Not long ago, the blog pages discussed in some detail issues related to sick leave and vacation pay. In these materials, I presented quite interesting opportunities that many did not know about or forgot. If you have not read these publications, you can also read them. This will be useful for both beginners and experienced users of the 1C ZUP software product.

Today we will look at how the program executes accrual for the time spent on a business trip, namely the document. This will be a kind of continuation of the previously mentioned materials and it will also be useful for experienced users of 1C ZUP, since I will be analyzing complex examples of accruals. In the examples, we will look at two options for paying for business trips in which the employee worked on weekends/holidays:

- Single payment based on average earnings (using "Individual schedules");

- Double payment (using document “Payment for holidays and weekends of the organization”).

A little theory

✅

✅

✅

The concept of a business trip is quite clearly stated in Labor Code of the Russian Federation in article 166: “ Business trip- a trip of an employee by order of the employer for a certain period of time to carry out an official assignment outside the place of permanent work. Business trips of employees whose permanent work is carried out on the road or has a traveling nature are not recognized as business trips.”

I will also highlight the position of the article 167 Labor Code of the Russian Federation: “When an employee is sent on a business trip, he is guaranteed to retain his place of work (position) and average earnings, as well as reimbursement of expenses associated with the business trip.”

Options for calculating travel allowances arise if business travel days fall on weekends or holidays. If work on weekends or holidays was not initially provided, then work on such days on a business trip is subject to wages double - article 153 Labor Code of the Russian Federation.

If work on weekends and holidays was provided for in advance and specified in the order or official assignment for a business trip, then such days are calculated based on average earnings.

Travel allowances based on average earnings + payment for work on weekends in a single amount (using “Individual schedules”)

✅ Seminar “Lifehacks for 1C ZUP 3.1”

Analysis of 15 life hacks for accounting in 1C ZUP 3.1:

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step by step instructions for beginners:

So, according to the conditions of the example, the chief equipment maintenance engineer for our car service center was sent on a business trip to a neighboring city, where they are preparing to open a branch, to help set up the equipment. The business trip is designed for 10 days - from 08/04/2014 to 08/13/2014. At the same time, work is planned on Saturday (09.08) and Sunday (10.08). In connection with this, the employee’s planned work schedule for August is changing, which in all previous months of his work was unchanged - a 40-hour five-day week.

First of all, we will enter an individual schedule for this employee for August 2014. For this we will use the document “Entering individual work schedules for an organization”. It can be found on the program desktop on the “Payroll” tab in the middle column. In the document we indicate the month of August and add a new row in the tabular section in which we select employee Gavrilov. In this case, the line will be filled with information about the planned schedule of this employee. We will set 8 hours of working time in the cells for August 9 and 10. In this case, upon returning from a business trip, the employee will be given days off on Friday and Saturday. Therefore, we remove the eights in the cells for August 14 and 15. We carry out the document.

Next, if the organization maintains detailed personnel records, then we create a document for the personnel records subsystem "Organizational business trips." This document does not calculate amounts, but is a personnel document - it must be entered by an employee of the personnel department. It can be found on the program desktop on the “Personnel Accounting” tab.

You can open this processing by clicking on the “Open accruals” button in the personnel document "Business trips of organizations".

So, let’s create, calculate and post the document “Payment based on average earnings.” Let's open it and see what the program has calculated for us. Thanks to the use of the “Analysis of No-Shows” processing, all fields were filled in automatically and the calculation was made.

To analyze the calculated amount, it is convenient to open the printed form of this document - "Calculation of average earnings".

Please note that since the employee was hired by the organization on January 1, 2014, income was taken into account not for 12 months as expected, but for 7. In addition, the working days of July were not fully taken into account since the employee was on vacation for half a month. So, the calculation of travel allowances is carried out according to the formula:

Average_daily_earnings * Number_of_days_of_business trip = Income_for_the_calculation_period / Counted_days_of_the_calculation_period * Number_of_days_of_business trip = 229,782.61 / 130 * 10 = 17,675.60

The program took into account exactly 10 days of a business trip since we introduced an individual schedule, where Saturday and Sunday falling on a business trip are marked as working days.

Travel allowances based on average earnings + double pay for work on weekends (document “Payment for holidays and weekends of the organization”)

✅ Seminar “Lifehacks for 1C ZUP 3.1”

Analysis of 15 life hacks for accounting in 1C ZUP 3.1:

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

So, let's change the conditions of our example a little. Employee Gavrilov went on a business trip on the same dates, but work on Saturday and Sunday was not expected. Already on the spot, it was decided that it was necessary to go out on weekends to resolve urgent issues. Consent was obtained from management.

Since it was not known in advance that the employee would have to work on weekends, his 40-hour five-day work schedule will not change (we will not use individual schedules). As in the previous example, we will enter a personnel document "Organizational business trips" on the basis of which we will create a settlement document "Payment based on average earnings" using processing "Analysis of no-shows". Let me remind you that you can read in detail about the use of this processing.

Let's open the created and calculated document "Payment based on average earnings" and analyze the amount received.

The average daily earnings did not change and this is correct, since we did not change anything in the billing period. But the payment amount has changed, since there are 8 business travel days at the time of calculating this document (Saturday and Sunday are days off as scheduled). From here we get: 1,767.56 * 8 = 14,140.48 rub.

Now you need to reflect the payment for work on weekends at double the rate. For this we will use the document “Payment for holidays and weekends of the organization.” The document should look like this:

In total, the document should contain 4 lines, two for each day. Payments are made according to two types of calculations "Payment for work on holidays and weekends" And “Additional pay for working on holidays and weekends.” It is better to fill it out manually. In this case, the data in the “Hourly tariff rate” field is calculated automatically by the program. Setting up options for calculating this indicator is carried out in "Accounting parameters" on the bookmark "Calculation algorithms" in a switch group “When converting the monthly salary into an hourly rate, use:”. I discussed these settings in detail in the corresponding article. The “Result” field is also filled in automatically based on the results of the data in the “Hours worked” and “Hourly tariff rate” fields. We carry out the document.

Let's summarize. Both examples essentially reflect two options for working on a day off, which are provided for by the Labor Code of the Russian Federation. The first example is essentially working for time off. An employee receives two days off upon returning from a business trip. The second example is double pay for work on a weekend.

This is the simplest example and therefore I will not illustrate it separately.

That's all for today! Soon there will be new interesting materials on.

To be the first to know about new publications, subscribe to my blog updates: